By John Ryan

The first part of this article concluded that the most likely cause of the Water Infrastructure Finance and Innovation Act (WIFIA) loan program’s dramatic decline from 2022 to 2024 was displacement by two other federally subsidized sources of U.S. water infrastructure finance, Clean and Drinking Water State Revolving Funds and tax-exempt water and sewer bonds. A big influx of IIJA funding possibly influenced the former, and normalizing interest rates were likely the driver of the latter. This second part will consider three implications of that conclusion, and what they indicate for renewing growth at this important loan program.

1. WIFIA’s Growth May Also Have Come from Displacement

If WIFIA’s declining loan volume 2022-2024 was due to changing exogenous factors favoring other financing sources, WIFIA’s rapid growth 2018-2021 might also have been due to exogenous factors favoring the program. Relevant conditions 2018-2021 appear, in retrospect, to have been quite positive for WIFIA loans, relative to the two other sources. During the period, SRF application lists grew longer while federal funding more or less flatlined, and atypical interest rates made WIFIA loans very competitive with tax-exempt water and sewer bonds.

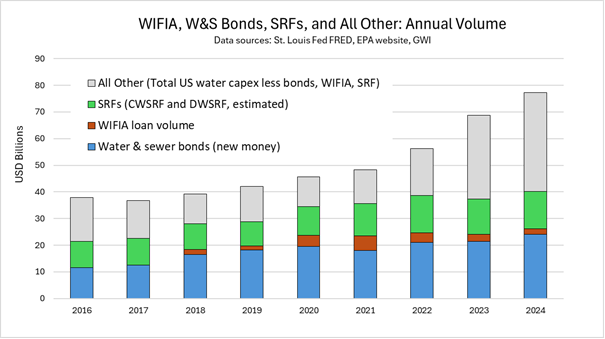

The chart above puts estimated financing volume from all three sources in the context of total U.S. water capital expenditures (capex). Overall financing from the sources was roughly 72% of total water capex during the 2018-2021 period, with slight annual variations. SRFs held a generally steady share of this volume; perhaps they would have grown slightly faster if WIFIA had not commenced operations in 2018? Bond volume lost ground relative to total capex, and in 2021 declined in absolute terms. WIFIA loan volume was the clear winner throughout the period.

Favorable conditions for WIFIA loans began to reverse in 2022 and volume declined thereafter, as described in Part 1 of this article. The impact of IIJA funding on total capex through direct grants significantly boosted the overall 2022-2024 trendline, but volume from the three sources stagnated, with bonds reclaiming share from WIFIA loans.

Overall, the chart paints a picture of three ‘products’ competing with each other for share in a relatively low growth ‘market.’ Most importantly, WIFIA’s commencement and rapid growth does not appear to have changed the total capex trend line 2017-2021. This suggests that program loans were not significantly additive in the context of its real-world policy purpose, increasing or accelerating US water infrastructure capex.

Part 1: Explaining the Decline in WIFIA Loan Volume

2. Many WIFIA Loan Features Overlap with SRFs and Bonds

Displacement as the primary reason for WIFIA’s growth and decline 2018-2024 implies that many WIFIA loan features overlap with those offered by SRF loans and bonds.

This was apparently widely understood at the program’s outset. When WIFIA law was being developed in 2014, SRFs expressed concern that the new program would diminish their role. Although WIFIA proponents argued that the two sources would only be complementary, a requirement that WIFIA offer a ‘right of first refusal’ to SRFs on project loans that qualify under both was included in the final statute.

For tax-exempt bonds, the original concern was that WIFIA loans would cause an increase in bond issuance to provide the balance of senior debt in new projects, thereby reducing federal tax revenue. Since this was viewed with the presumption that WIFIA would enable projects that otherwise would not have proceeded, competition between the two sources was not considered, at least not publicly. But it does suggest an understanding that WIFIA loans and bonds play a similar role in project capitalization.

WIFIA’s actual results 2018-2024, when seen in the context of the two other sources and total water capex, appear to confirm the early recognition of potential overlap, especially with bonds. Interestingly (or ominously), in May of this year, the White House FY 2026 Budget Summary justified proposed cuts to SRF funding by asserting “the SRFs are largely duplicative of the EPA’s [WIFIA] program.”

3. Displacement is Inconsistent with OMB Credit Program Policy

Whatever the intentions or expectations of WIFIA policymakers were in 2014, displacement as the explanation for much of WIFIA’s actual history 2018-2024 implies that the program has not been in strict compliance with the Office of Management and Budget’s standard policy for federal credit programs.

That policy is stated in detail in OMB Circular A-129, most recently updated in 2024. The first sentence of section 2 of the Circular says bluntly that “Federal credit assistance should be provided only when it is necessary…to achieve clearly specified Federal objectives.” The section goes on to require periodic review of the credit program with respect to a list of goals.

The description of one goal, relevant to SRF displacement, asks “Whether any Federal credit or non-credit program exists that addresses a similar need…” It could be argued that WIFIA was originally designed to provide larger loans than most SRFs and is better able to address the needs of large projects. But the program’s statute does include some exceptions for smaller loans. Perhaps more importantly, EPA press releases since 2021 have emphasized loans to smaller projects as a WIFIA priority, in effect indicating an intention to compete with SRFs.

“At this point, WIFIA can still be seen as a successful experiment.”

Though federally subsidized, tax-exempt bonds are of course issued and traded in a private market. Another Section 2 goal explicitly requires that “that private lending is displaced to the smallest degree possible by agency [credit] programs.” This requirement is hard to reconcile with the interaction of WIFIA loans and bonds 2018-2024, especially in 2021.

An Opportunity for Renewal: Redesigning WIFIA

Although this article has focused on WIFIA’s shortcomings, my goal is not to criticize. Rather, it’s to assess the reality of the program’s current position, for two reasons. The first is the level of risk that WIFIA might face under the current administration. This comes not from a fully developed policy towards federal water infrastructure finance, but from its absence. In a vacuum, ideologically motivated elements in the government can ask hard questions (e.g., about OMB Circular A-129 compliance) and promote a case against a program they oppose for whatever reason. WIFIA stakeholders should be asking those questions first – and develop answers.

Second, WIFIA’s decline 2022-2024, combined with the policy vacuum mentioned above, represents an opportunity to improve the program and renew its growth. At this point, WIFIA can still be seen as a successful experiment. Its 2018-2024 history shows that a federal loan program can efficiently and effectively deliver large-scale project financing for U.S. water infrastructure, a critical capability for U.S. water infrastructure improvement. That history also shows that if displacement and overlap among WIFIA, SRFs and the tax-exempt bond market can happen, it will happen, and real-world policy outcomes will not be achieved. Now we have seen what works – and what doesn’t. The program is clearly worth preserving, but it clearly requires redesign.

Since WIFIA’s overall structure has worked well, redesign can be narrowly focused. If zero-sum displacement with two other sources of federally supported finance was the primary cause of WIFIA’s shortcomings, differentiating WIFIA loans from SRF loans and tax-exempt bonds by statutory amendment of program loan features is a straightforward solution.

WIFIA: Examining Synergies with the Muni Bond Market

The overall goal of the amendments is, of course, to increase U.S. water infrastructure construction and renewal – WIFIA loans should be additive. Loan features that help water agencies facilitate local funding in ways that improve affordability for the community while minimizing transfer payments from federal taxpayers is the specific aim. Other priorities for amendment design should include:

- Utilization of intrinsic federal lending strengths, relative to other financing alternatives.

- Predictably low (or zero, where possible) cost to federal taxpayers.

- Potential synergies with other sources of federally supported water finance through proactive engagement and joint development with those sources, especially tax-exempt bonds.

Immediate action is possible. The 55-year WIFIA loan term for long-lived projects in the recently re-introduced Water Infrastructure Finance and Innovation Act (WIFIA) Amendments of 2025 is an example of effective and practical differentiation. WIFIA program stakeholders and water sector advocacy groups should strongly support its enactment.

John Ryan is principal of InRecap LLC, focused on debt alternatives for the recapitalization of basic public infrastructure. Ryan has an extensive background in structured and project finance, and recently served as an expert consultant to the U.S. EPA. He is a frequent contributor to WFM on EPA’s WIFIA loan program and related topics.

There are going to be some apples to oranges comparison problems since WIFIA is a federal program with one structure and SRF refers to 50-100 different state programs (DW, CW).

Maybe comparing WIFIA to USDA is a better study?

In NC, there are tremendous needs in small towns. Small towns can use SRF if principle forgiveness is offered at a significant ratio to general loan. Small towns CANNOT use WIFIA, meant for big projects, strictly a loan, and requiring a match.

My theory on WIFIA… there is no more market for the product. The potential project list for something in the $100 million range is small. Big utilities have either gone down the path and gotten a WIFIA loan to fund their big things, or they struggle with the compliance burden and cost risk.

If the compliance burden and cost risk were reduced, I predict wifia would once again get traction. And, if there was a way for WIFIA to mirror the terms of SRF money at 2-4% without cost match, small towns would jump on the chance to get money for their sub-$5 million projects.

Well, SRF advocacy groups thought the comparison was close enough to express concern & get a right of first refusal included in the WIFIA statute in 2014, as noted in the article.

If the data was available, I would have broken USDA lending out of All Other. I’m guessing it would roughly have tracked SRF volume on a smaller scale – same small project focus.

Re WIFIA for smaller projects, see my reply to your comment to Part 1 of the article.

Didn’t know you replied! Didn’t remember commenting! Thanks for taking the time. Enjoyed the reading.