By John Ryan

What is happening at EPA’s Water Infrastructure Finance and Innovation Act (WIFIA) loan program?

The mysterious issue is not the near-complete cessation of loan closings under Trump 2.0. The reason for that is clearer: the Office of Management and Budget’s pause on federal grants and loans in February combined with continuing federal upheaval under this administration.

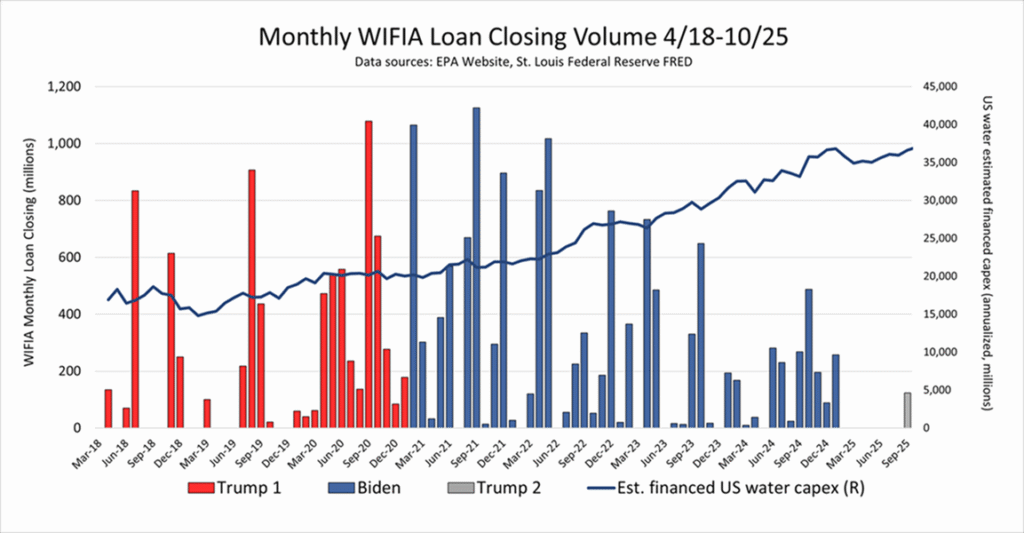

Much harder to explain is the steady decline in program loan volume since the end of 2021 through January 2025, despite rising U.S. water sector capex. During this period, WIFIA had a supportive Biden administration, plenty of funding and was run as efficiently as ever. Yet, the program’s annual executed loan volume fell from a calendar year peak in 2021 of over $5.5 billion to under $2 billion in 2024.

This dramatic, 63% decline is likely to have important policy implications. This article, the first of this two-part series will outline four possible causes. Part 2 in the coming weeks will consider the implications and what actions U.S. water sector stakeholders and policymakers can or should take.

Possible Reason 1: Apparent Decline is a Statistical Anomaly

Perhaps the premise of ‘decline’ is unwarranted? The monthly volume chart appears to show rising and falling trends, but the data set is small (only 140 loans in total) and the time scale is relatively short. It is possible that the apparent trends are not statistically significant.

However, in a real-world context of near-term challenges, the decline is significant enough to cause concern. Two factors are especially important:

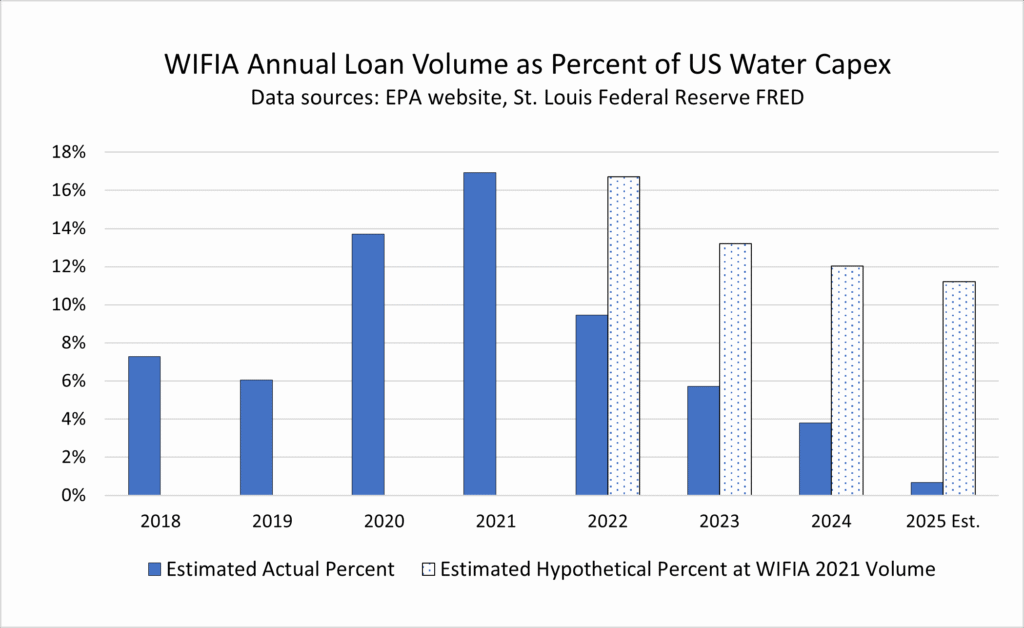

First is the scale of decline in contrast to growing demand in U.S. water capex. The important reference point for a federal program is not its growth (or lack thereof), but outcomes relative to the problem it exists to solve. In those terms, WIFIA’s decline is even more dramatic, from a ‘market share’ of financing about 17% of U.S. water capex in 2021 to under 4% in 2024. Even if WIFIA 2021 peak volume remained steady at $5.5 billion, the decline in ‘market share’ would still be pronounced, as the chart below shows.

The second important factor is that perception matters. Regardless of statistical significance, the numbers and graphics depicting WIFIA loan volume since 2021 are dramatic. In political conditions where ideology can drive otherwise purely technocratic policy decisions, perception is the reality. Arguably, we are in that type of situation now, and likely will remain so for at least three more years.

Possible Reason 2: Rising Long-Term Rates

Long-term interest rates started rising off historic lows in 2020, but the pace and trajectory solidified by the end of 2021. Perhaps project sponsors increasingly turned to other, non-debt, sources of capitalization?

This is generally implausible because of the scale and steady rise in U.S. water capex. It’s also unlikely because inflation was often higher than interest rates, and there was uncertainty about where the rise would end (i.e., that rising rates might be a reason to lock in current rates).

More specifically, higher rates did not affect a comparable source of finance. WIFIA loans and muni bonds are similar in many fundamental ways from the borrower’s perspective. Both are long-term, fixed rate, amortizing, secured debt that can be done in large scale for investment-grade project borrowers. Both are federally subsidized. Most importantly, the vast majority of WIFIA’s borrowers are highly rated public water agencies that generally issue in the tax-exempt muni market as well. Yet, tax-exempt municipal bond issuance did not experience a significant decline in the period. Volume dipped slightly in 2022, held steady in 2023 and surged in 2024, with 2025 on track to be a record year.

Possible Reason 3: Influx of IIJA Funding for SRFs

The Infrastructure and Investment Jobs Act (IIJA), enacted at the end of 2021, provided about $44 billion in new funding for U.S. water infrastructure through the EPA’s State Revolving Funds (SRFs). Could IIJA funding have depressed WIFIA loan demand?

This seems plausible. The timing fits the beginning of WIFIA volume decline, and scale of new funding was very significant in the context of U.S. water capex. Although actual allocation and obligation of the funding has been slow, the perception of its eventual availability could have had an immediate impact on WIFIA loan demand.

However, direct evidence of an impact is hard to find. As noted above, tax-exempt bond volume was apparently not significantly affected. Also, since SRFs mainly provide financing and grants for smaller, less creditworthy projects, displacement should have caused average WIFIA loan size to increase. In fact, average program loan size steadily decreased, from $461 million in 2021 to $165 million in 2024.

Possible Reason 4: Relative Cost of a WIFIA Loan vs. Tax-Exempt Municipal Bond

As noted above, WIFIA loans and tax-exempt muni bonds are structurally similar. Perhaps project borrowers were actively choosing between these two types of senior project financing throughout the program’s operational period 2018-2024? WIFIA volume trends, both rise and fall, would then reflect how changing conditions impacted the relative value of the two alternatives.

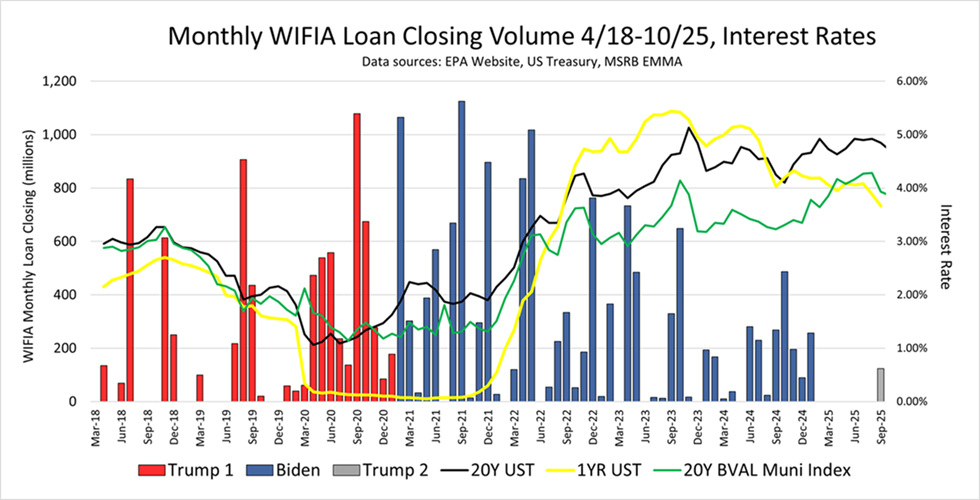

There are two observable factors in the cost of each financing alternative which are relevant to most if not all projects deciding between WIFIA loans and muni bonds: The cost of interest and the cost of locking in permanent financing rates during project construction. The former is reflected in U.S. Treasury yields (on which WIFIA rates are based) and in market indices of high-quality municipal bonds. The latter is primarily influenced by the difference between short-term and long-term rates.

The chart below overlays the 20Y UST, 20Y muni index rates, and 1Y UST rates on WIFIA monthly loan volume:

As a general observation, WIFIA volume appears roughly correlated with (1) the closeness of the 20Y UST and the 20Y muni index rates, and (2) the positive difference between the 20Y muni index and 1Y UST rates, as an indicator of yield curve steepness. From 2018 to the beginning of 2020, UST and muni index rates were atypically close, and the yield curve was roughly normal, both factors favoring WIFIA loans. In 2020 the factors favoring WIFIA were even more pronounced, becoming less so but still favorable in 2021 to early 2022.

From early 2022 through 2024, however, cost factors became markedly unfavorable for WIFIA loans. The muni bond index normalized below WIFIA’s UST rates, and the yield curve became very inverted.

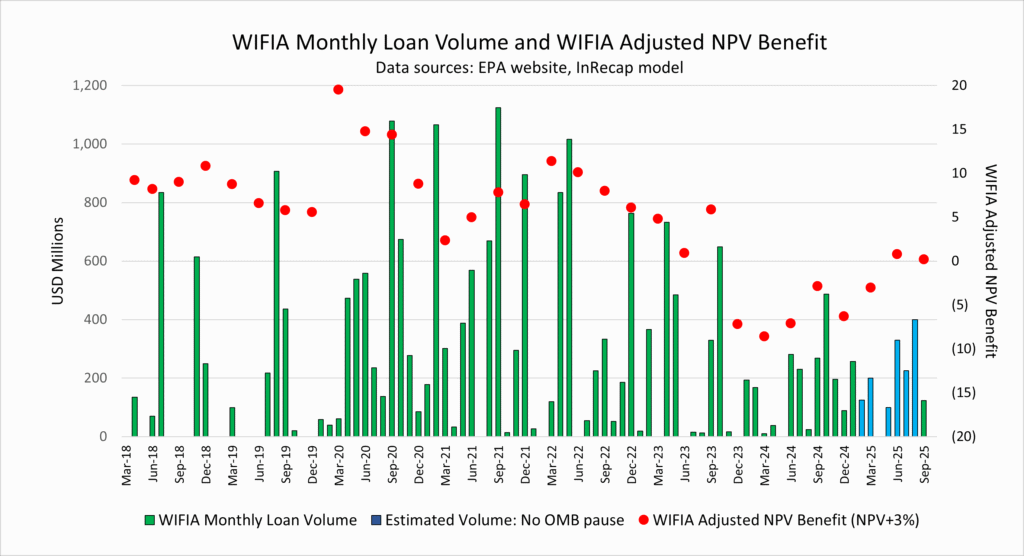

A more detailed analysis can incorporate full rate curves, credit spreads and other information to estimate the net present value (NPV) cost of each alternative. The difference between the NPV cost of a bond issue and a comparable WIFIA loan financing for a typical project, as adjusted for certain WIFIA non-NPV features, is the ‘WIFIA Adjusted NPV Benefit’. It is shown for 2018-2025 in the chart below, overlaid on WIFIA monthly volume:

Apparent trends in WIFIA Adjusted NPV Benefit appear to track actual trends in monthly volume relatively closely. Intuitively, when the Adjusted NPV Benefit is very positive, WIFIA not only gets more applications but more applicants already in the pipeline will press harder to close. When less positive or even negative, fewer projects will apply or press to close.

The chart adds a hypothetical volume for 2025, based on the Adjusted NPV Benefit, as if the OMB pause and Trump’s second administration had not occurred. The hypothetical volume for all of 2025 would probably have been about $1.7 billion, representing continued decline, though at a slower pace than in 2022-2024.

Summary

- WIFIA loan volume decline is significant enough, especially in the context of growing US water infrastructure needs, for stakeholders and policymakers to be concerned.

- The overall rise of long-term interest rates over 2022-2024 does not provide an explanation for the WIFIA decline. Specifically, volume in tax-exempt bond market did not show a decline in the period.

- Some impact from IIJA funding for SRFs on WIFIA loan volume is likely, but its scale or nature is unclear.

- The relative value of WIFIA loans compared to tax-exempt municipal bonds appear to explain much of the trends in WIFIA loan volume for its entire operational history, 2018-2025.

Part 2 of this article will consider the policy implications of the trends and likely causes of WIFIA loan volume decline from 2022 to 2024.

John Ryan is principal of InRecap LLC, focused on debt alternatives for the recapitalization of basic public infrastructure. Ryan has an extensive background in structured and project finance, and recently served as an expert consultant to the U.S. EPA. He is a frequent contributor to WF&M on EPA’s WIFIA loan program and related topics.

Any chance WIFIA might programmatically change? It seems like only the largest utilities have access to this tool.

Could the decline be just that WIFIA is reaching the true SOM in a much larger TAM?

I hope so – see Part 2 online now.

Federal strengths as an infrastructure lender are – realistically – best deployed for large projects. Small projects trip up federal weaknesses – risk evaluation, bureaucratic cost diseconomies, etc. SRFs much better positioned for that.

But I think WIFIA should support small projects indirectly with large loans to pools or portfolios of small projects. There should be a lot more focus on SWIFIA e.g., https://waterfm.com/revisiting-wifia-sub-ust-interest-rates-for-srfs/

WIFIA’s eligibility statutes could be refined to support self-organizing co-ops of small projects – this post on CWIFP for small dams, but can be generally applied: https://www.inrecap.com/?p=2794

Re SOM/TAM – if WIFIA were a small private bank, yes maybe a specialized niche player. But as a federal program – what’s the policy objective? Plenty of infrastructure finance is needed. However, I do agree that some sort SOM/TAM perspective is required re interaction with other type of federally supported finance – Part 2 talks about that.

Missing two key points:

1) WIFIA purposefully went after big projects in its early years to show its benefit and while it still there for that after being established for a while it also went after smaller municipalities with smaller projects to show it’s capable and useful for all credit worthy municipalities with projects of 5M or greater.

2) You’re also forgetting to factor federal requirements. AIS was already a headache, then in 2022 BABA began to be required and while it didn’t end up impacting many WIFIA projects until later the perception that all permanently constructed materials had to be made in the US would be such a logistics nightmare and add significant cost in addition to the alternative financing available made it a less attractive option despite its wonderful flexibilities.

Re (1) – see Part 2. There was a ‘narrative shift’ at EPA to smaller projects around 2021, but I think that was mainly political aspiration as opposed to a real change in implementation. Average loan size in 2024 was still around $165m (i.e., $320m project). As for WIFIA’s potential role for small projects, see reply to the prior comment.

Re (2) Yes, all the red tape, policy riders, crosscutters – AIS, NEPA, Davis-Bacon etc. etc. definitely depress demand & make the program less useful. But all that was there from the beginning in 2018 – what changed so dramatically in 2022-2024 to cause a 63% decline? You’re aware that BABA requirements were waived in May 2022 for projects that had begun planning prior to then – that would have applied to most (if not all) projects seeking to close on project financing commitments 2022-2024.

But I agree w/ your general point – in addition to amending loan features, all the federal requirements that don’t contribute to the policy goal – more water infrastructure – should be revisited & culled wherever possible.